Joby’s Dream and Flying Cars

The Patents Are Clever. The Physics Don’t Care.

I. EXECUTIVE SUMMARY

Joby Aviation is attempting something that has never been done: build a commercially viable, hydrogen fuel cell-powered eVTOL aircraft, certify it under regulatory frameworks that do not yet exist, and bring it to market before the company’s cash runway expires. We are short JOBY.

The company trades at a $9.5B market capitalization — roughly the same as American Airlines, which flies 200 million passengers a year on nearly 1,000 aircraft. Joby has never flown a paying passenger. It has never certified an aircraft. Its hydrogen fuel cell eVTOL exists, as of this writing, primarily as a portfolio of patents and a burn rate.

This report is built on three categories of public evidence: Joby’s own USPTO patents, the peer-reviewed engineering literature on hydrogen fuel cell aviation, and the FAA’s regulatory documents — cross-referenced against Joby’s SEC-filed financials. What they show, taken together, is a company that must simultaneously double the state of the art in fuel cell power density, solve cryogenic engineering problems that defeated the Space Shuttle program’s budget, certify an aircraft under frameworks that do not yet exist, build hydrogen infrastructure at airports where none exists, retrofit parking garages into vertiports requiring substation-level electrical feeds and FAA airspace certification, and do all of it while burning over $500M per year with roughly 18 months of cash runway remaining.

The patents show genuine engineering depth. The thermodynamic integration is clever, the weight-reduction architectures target the right subsystems, and the inventors clearly understand the literature. But clever patents are not demonstrated hardware. And demonstrated hardware is not a certified aircraft.

What follows is organized into ten sections. We begin with the cash and the valuation — because no matter how elegant the engineering, physics operates on the investor’s timeline only if the money lasts long enough. Then we walk through seven technical, regulatory, and infrastructure challenges, each independently formidable, and explain why they cannot be solved sequentially: they interact, they trade off against each other, and they must all be resolved simultaneously in a system where the acceptable failure rate is measured in events per billion flight hours.

The bull case requires believing Joby has solved, or has a credible near-term path to solving, all of them. The bear case notes that the insiders closest to that answer have been selling stock every month.

II. THE CASH BURN PROBLEM

Before we get to the engineering, we need to talk about the clock. Every technical challenge in this report exists under a constraint that the market appears to be ignoring: Joby is a pre-revenue company burning cash at an accelerating rate, and the runway is shorter than it looks.

The Numbers

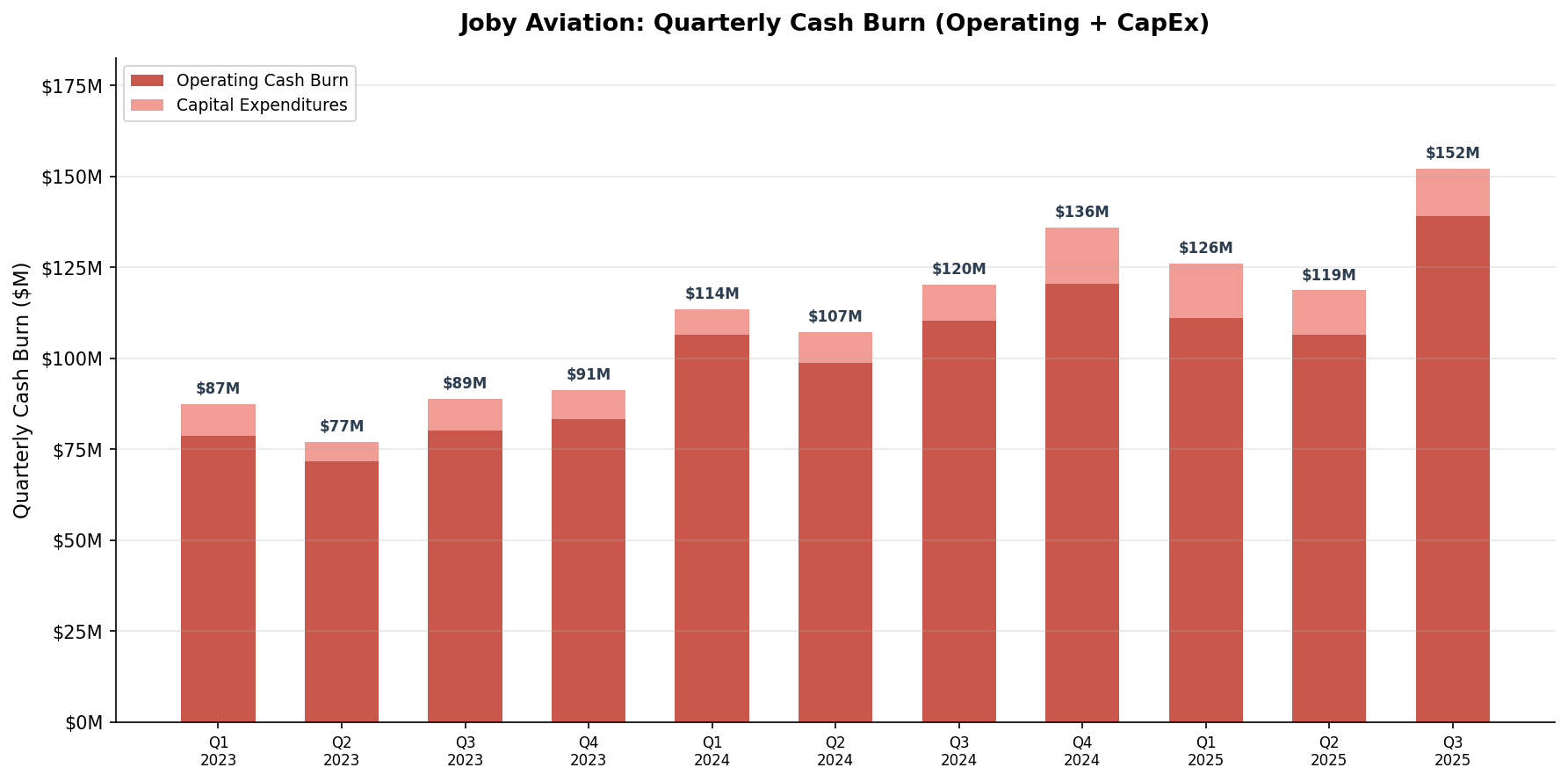

The following table is derived from Joby’s SEC-filed quarterly financial statements (10-Q and 10-K). Operating cash burn is net cash used in operating activities; capital expenditures are payments to acquire property, plant, and equipment. Total burn is the sum of both.

| Quarter | Operating Burn | CapEx | Total Burn | Liquidity (Cash + Investments) |

|---|---|---|---|---|

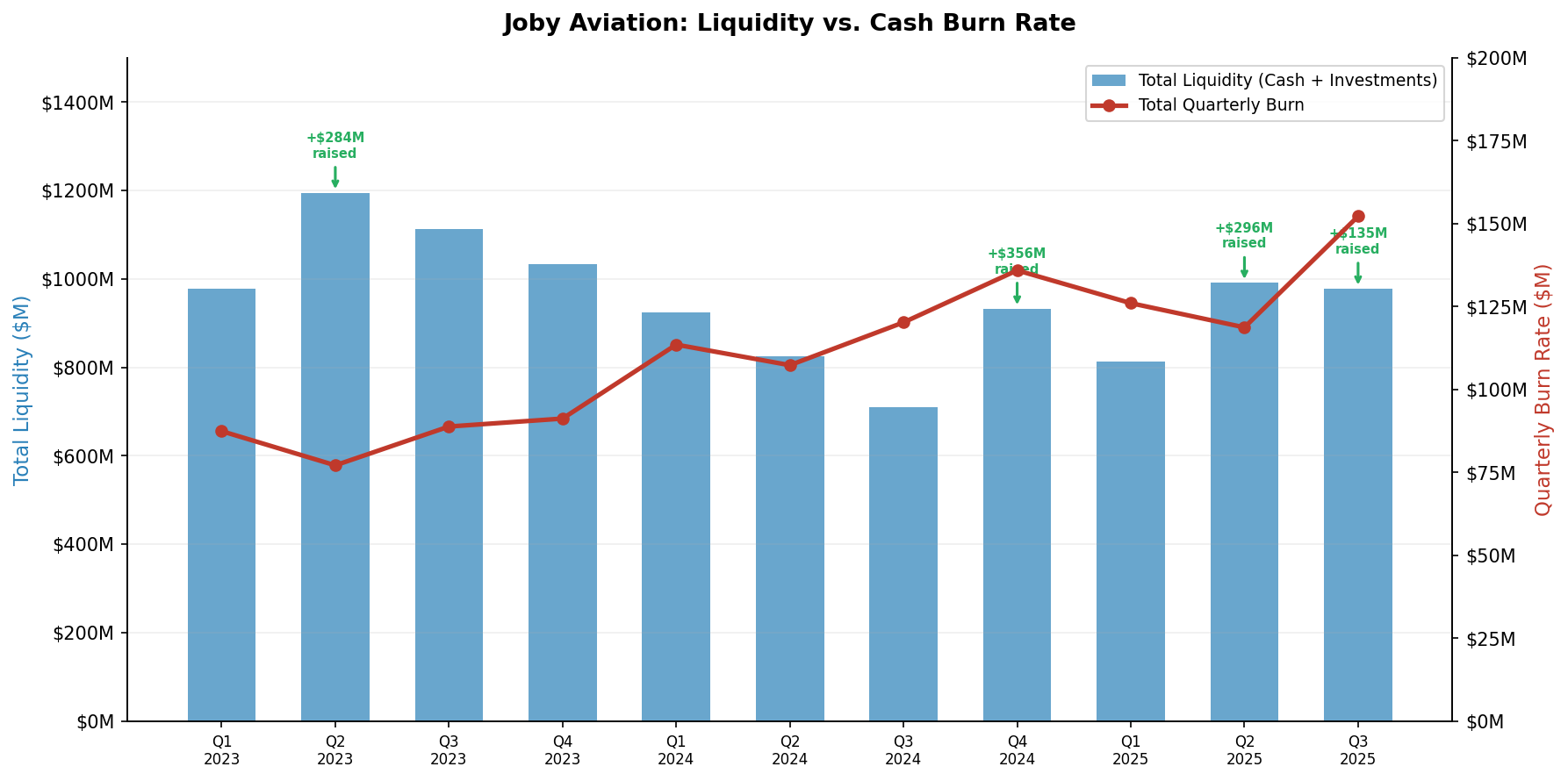

| Q1 2023 | $78.6M | $8.8M | $87.4M | $977.8M |

| Q2 2023 | $71.7M | $5.4M | $77.1M | $1,194.8M |

| Q3 2023 | $80.2M | $8.6M | $88.8M | $1,112.5M |

| Q4 2023 | $83.3M | $7.9M | $91.2M | $1,032.3M |

| Q1 2024 | $106.6M | $6.9M | $113.5M | $923.9M |

| Q2 2024 | $98.8M | $8.5M | $107.3M | $825.0M |

| Q3 2024 | $110.3M | $9.9M | $120.2M | $710.0M |

| Q4 2024 | $120.5M | $15.4M | $135.9M | $932.9M |

| Q1 2025 | $111.0M | $15.0M | $126.0M | $812.5M |

| Q2 2025 | $106.6M | $12.1M | $118.7M | $991.0M |

| Q3 2025 | $139.2M | $13.0M | $152.2M | $978.1M |

Two things jump out of that table. First, the burn rate has nearly doubled — from $87M per quarter in Q1 2023 to $152M in Q3 2025. Second, the liquidity column only stays above $900M because Joby keeps raising capital. Strip out the equity raises and the trajectory is a straight line down.

Quarterly cash burn (operating + CapEx) from Q1 2023 through Q3 2025. The trend is clear: burn has nearly doubled over eleven quarters, driven primarily by accelerating operating expenses as Joby scales R&D, headcount, and manufacturing preparation. CapEx has also roughly doubled as the company invests in production tooling and facilities.

The Dilution Treadmill

Joby’s liquidity hasn’t collapsed because the company has been raising capital aggressively. Since Q2 2023, Joby has tapped equity markets four times for a combined ~$785M in financing cash flows — $284M in Q2 2023, $356M in Q4 2024, $296M in Q2 2025, and $135M in Q3 2025.

The cost of this capital is dilution. Shares outstanding have grown from 630M to 874M — a 39% increase in under three years. Every raise keeps the lights on for another few quarters while spreading the company’s speculative value across a larger share base.

Total liquidity (cash + short-term investments, blue bars) versus quarterly burn rate (red line). The green annotations mark significant capital raises. Without those raises, liquidity would have been exhausted by mid-2025. The burn rate line continues to climb while the raises grow more frequent.

The Runway Math

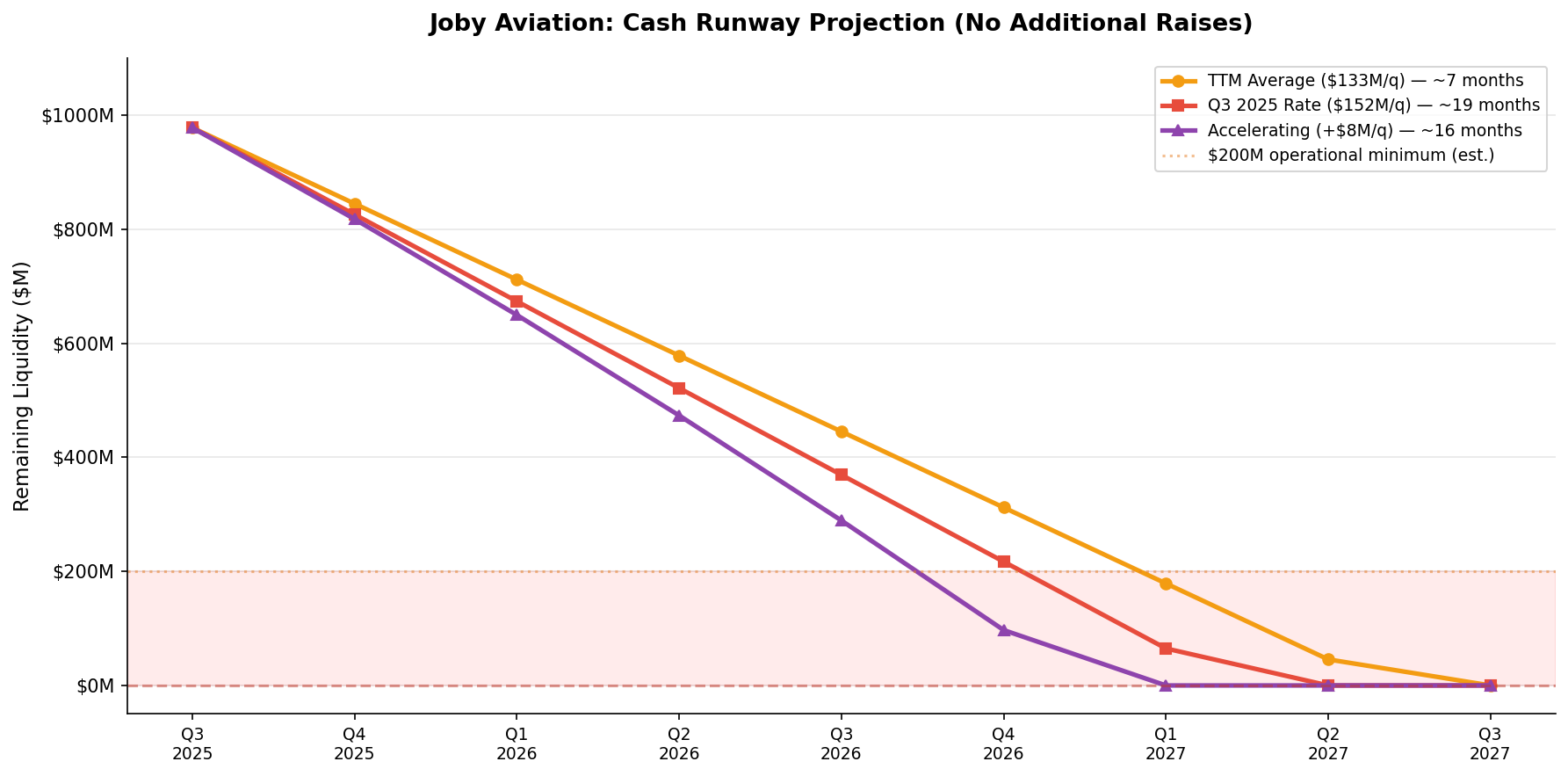

As of September 30, 2025, Joby held $978M in cash and short-term investments. The question is how long it lasts. The answer depends on which burn rate you use — and the trend is not in Joby’s favor.

Cash runway projections assuming no additional capital raises. The orange line uses the trailing-twelve-month average burn of $133M/quarter (~$533M/year), giving roughly 22 months. The red line uses the most recent quarter’s $152M rate, giving roughly 19 months. The purple line assumes the burn continues accelerating at +$8M/quarter — consistent with the 2023-2025 trend — giving roughly 16 months. The shaded red zone below $200M represents an estimated operational minimum below which the company cannot function.

Three scenarios, one conclusion:

- At the TTM average (

$133M/quarter,$533M/year):~22months of runway from September 2025, or roughly mid-2027. - At the most recent quarter’s rate (

$152M/quarter,$608M/year):~19months, or roughly April 2027. - At the accelerating trend (

+$8M/quarter):~16months, or roughly January 2027 — before Joby’s first hydrogen aircraft could plausibly complete FAA certification even under the most optimistic timeline.

The practical number is somewhere around 18 months. And “practical” is generous, because a company cannot operate down to zero — below some threshold (we estimate $200M), Joby loses the ability to fund operations, make payroll, and maintain supplier relationships. The usable runway is shorter than the mathematical runway.

What This Means

Joby will need to raise capital again. Probably more than once. Each raise dilutes existing shareholders and depends on the market’s willingness to fund a pre-revenue company with accelerating losses. That willingness, in turn, depends on the market believing the engineering challenges described in the rest of this report can be solved in time.

Revenue is not coming to the rescue. Through the first three quarters of 2025, Joby reported $22.6M in total revenue — essentially a rounding error against $477M in operating cash burn over the same period. Even the most generous revenue projection cannot close a gap this wide before the runway expires.

The clock is ticking. Here is what has to happen before it runs out.

III. WHAT $9.5 BILLION IS PRICING IN

What Joby Has Today

Joby’s near-term response to the burn rate described above has two components: certify the S4 battery-electric eVTOL aircraft and acquire revenue.

In August 2025, Joby announced the acquisition of Blade Air Mobility’s passenger business for up to $125M.1 Blade operated helicopter and seaplane shuttle services from a network of 12 urban terminals — including dedicated facilities at JFK, Newark, and three Manhattan locations — flying more than 50,000 passengers in 2024.1 Blade’s medical division was not included in the transaction and remains a separate public company.

Joby did not buy Blade to run a helicopter company. It bought Blade’s route agreements, terminal leases, and landing rights — the infrastructure contracts that will allow Joby to slot its own aircraft into existing urban corridors once the S4 receives FAA type certification. The helicopters are a placeholder. The S4 is the replacement.

The S4 is a fully battery-electric eVTOL with a stated range of approximately 150 miles. At 150 miles, it serves the same short-hop routes that Blade already operates: airport transfers, city-to-suburb corridors, Manhattan to the Hamptons.

Why It Isn’t Enough

Blade’s passenger segment — the business Joby acquired — generated $102M in revenue in 2024.2 Short-distance helicopter shuttles accounted for $72M; jet charters and other services made up the remaining $30M.

Set that against Joby’s burn rate. In the most recent quarter, Joby burned $152M in cash. Annualized, that exceeds $600M. Blade’s $102M is not a floor Joby is building on — it is a ceiling the company is trying to reach again, with a different airframe, after spending years and billions of dollars to get the S4 certified. The revenue Joby has reported since the acquisition closed is Blade’s helicopter revenue. It is not eVTOL revenue. No passenger has ever paid to fly on a Joby aircraft.

In the best case — S4 certified, Blade’s helicopters replaced, full route network converted — Joby recaptures approximately $102M in annual revenue on the same short urban corridors Blade was already serving. That is a business worth what Joby paid for it: $125M. It is not a business worth $9.5B.

What the Valuation Actually Requires

Joby trades at approximately $9.5B — roughly the same market capitalization as American Airlines, which operates nearly 1,000 aircraft, employs approximately 130,000 people, flies 200 million passengers per year, and generated approximately $54B in revenue across 2024.3

Working backward from the market cap reveals the scale of what the valuation implies. Airlines trade at approximately 0.15x–0.3x revenue. Even granting Joby a generous 3x technology premium — a multiple typically reserved for high-growth software companies, not capital-intensive transportation — a $9.5B market cap requires roughly $3B in annual revenue at maturity. Blade’s passenger business is 3% of that number.

What does $3B in annual revenue look like? At $200 per seat with four passengers per flight, each revenue flight generates approximately $800. That means 3.75 million revenue flights per year — over 10,000 flights per day, every day. At an optimistic utilization of 15 flights per aircraft per day, that requires a fleet of approximately 700 aircraft in daily commercial operation — all FAA type-certified, all operating from purpose-built vertiports, all flying under airworthiness standards that do not yet exist.

The gap between $102M and $3B is hydrogen. Hydrogen fuel cells are what extend range from 150 miles to 500+ miles. They are what make routes like New York to Washington, Los Angeles to San Francisco, and cross-Gulf-state corridors possible without a runway. They are what transform Joby from Blade with a better airframe into a regional air mobility platform connecting every major city in America — the only category large enough to generate $3B in annual revenue.

The Manufacturing Ramp That Doesn’t Exist

Even if every engineering and certification challenge in this report is resolved, the path from zero to 700 aircraft in commercial service requires a production ramp without precedent in novel aviation. Conventional programs take 5–10 years to move from initial type certification to mature delivery rates — and that timeline assumes an existing supply chain and manufacturing base. Airbus ramped A320neo production from first delivery in 2016 to approximately 50 per month only by 2024, and that was for a derivative of an existing design with decades of supplier relationships. Joby must build this entire capability from scratch, for a first-of-its-kind hydrogen fuel cell aircraft, while simultaneously constructing hydrogen infrastructure, vertiport networks, pilot training programs, and maintenance organizations across multiple cities.

Every technical challenge in the sections that follow is a direct consequence of this dependency. The battery-electric S4 is the certification vehicle — the near-term proof that Joby can build and certify an eVTOL. Hydrogen is the business case — the technology that unlocks the route economics the valuation requires. The $9.5B bet is not on the aircraft Joby is building today, but on the aircraft it must build next.

IV. THE POWER DENSITY BARRIER

What Joby Is Trying to Do

To understand Joby’s hydrogen bet, you need to understand one number: 2 kW/kg.

That is the fuel cell system specific power — watts of electrical output per kilogram of total fuel cell system weight — that a 2023 MIT analysis by Cybulsky et al.4 identified as the minimum threshold for commercially viable hydrogen-powered regional aviation. Below 2 kW/kg, the fuel cell system is so heavy that it eats into the aircraft’s payload budget until there is no room left for passengers. Above it, the math works. Doubling specific power from 1 kW/kg to 2 kW/kg decreases the required payload reduction from 58% to 8% for a 1,000 nautical mile range — the difference between a demonstrator that flies empty and an aircraft that can actually carry people.

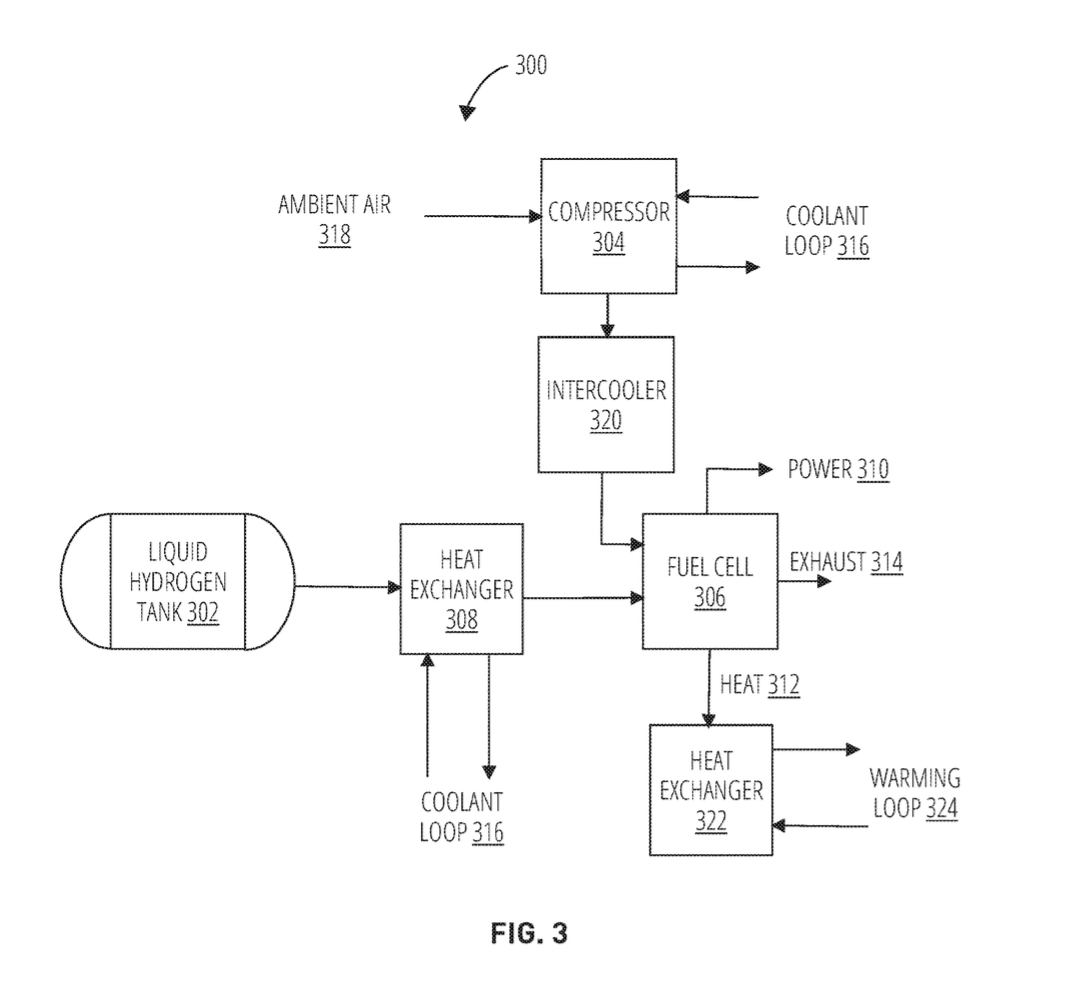

Joby’s foundational fuel cell patent5 describes a thermodynamic system designed to hit that number. It treats liquid hydrogen’s extreme cold (-253°C) not merely as a storage challenge but as a thermodynamic resource. Compressed inlet air is pre-cooled using the hydrogen’s cold, the hydrogen’s pressure drop from cryogenic storage to fuel cell inlet is captured as work via an expansion turbine, and waste heat from the fuel cell is recovered and directed back into the system.

The architecture is consistent with what the MIT analysis says is necessary. The question is whether it can be built.

Where the Industry Actually Stands

The gap between current capability and Joby’s required target is substantial.

A fuel cell system has two major weight components. The stack — the electrochemical cells themselves — has achieved approximately 4 kW/kg in PEM (proton exchange membrane) configurations.6 That sounds like it exceeds the 2 kW/kg target by a wide margin. It does not, because a stack alone cannot power an aircraft.

Around the stack sits the balance of plant: an air compressor to feed oxygen, a thermal management system to reject waste heat, cooling loops, water management to prevent membrane flooding or drying, and power electronics to condition the output. This is where the weight lives. The UK Aerospace Technology Institute’s Fuel Cells Roadmap confirms that while PEM stacks have hit 4 kW/kg, the balance of plant drives total system-level power density down to approximately 0.65–1 kW/kg — the best demonstrated in automotive applications.6 NASA’s eVTOL fuel cell study set 1.1 kW/kg at the system level as the minimum target just to match piston-engine rotorcraft performance, identifying ultra-light stack cooling and short-term hydrogen storage as the two key development drivers.7

The gap: industry best is ~1 kW/kg at the system level. Joby needs 2 kW/kg. They need to roughly double the state of the art.

Joby’s Architectural Response

Two subsequent patents reveal how Joby is attempting to close this gap. Both target the balance of plant directly — the exact subsystem the literature identifies as the barrier.

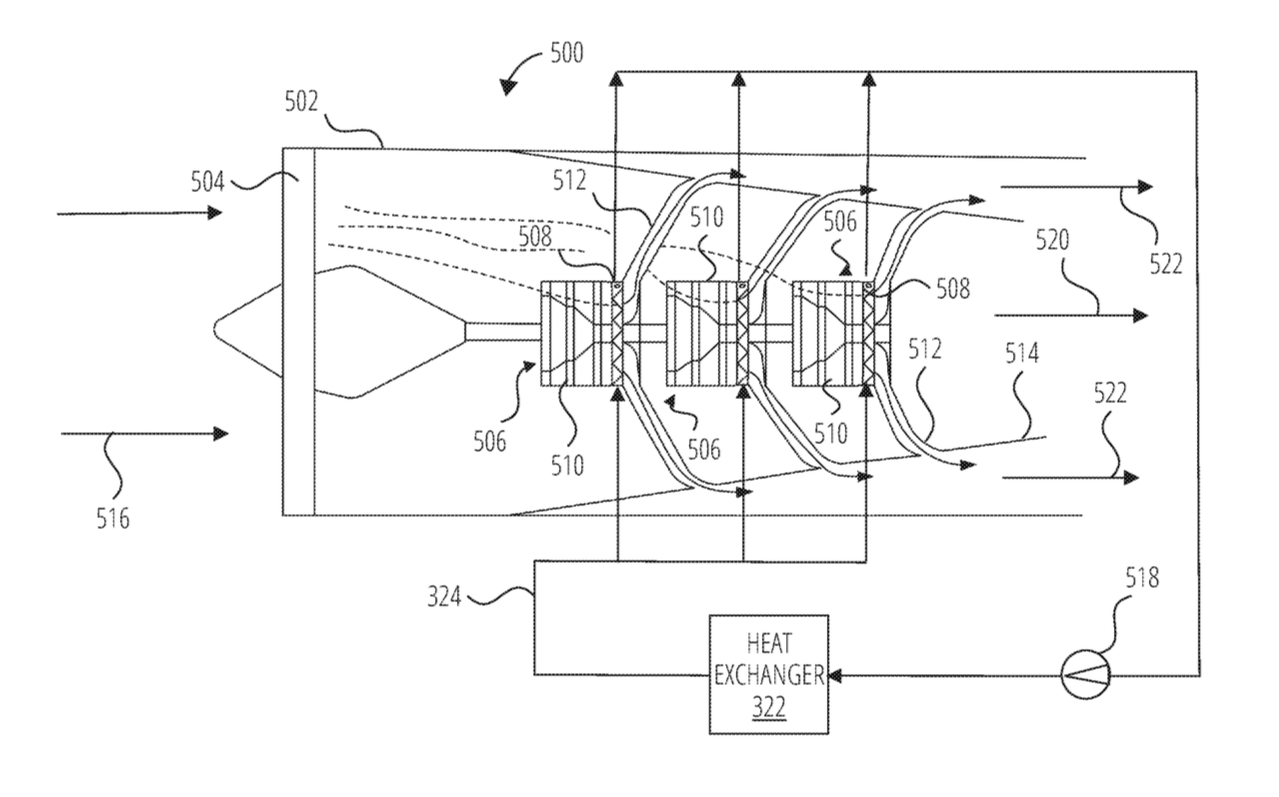

The first targets the cooling system.8 The proposed design eliminates the traditional cooling radiator entirely by routing fuel cell coolant through a heat exchanger located inside the propulsor fan duct. The fan pulls air through the duct; the heat exchanger dumps fuel cell waste heat into that airflow; diffuser vanes downstream and a variable area nozzle recover thrust from the heated air. Dead-weight cooling hardware is replaced by a system that simultaneously cools the fuel cell and generates thrust.

System-level thermal flow diagram from Joby’s duct-integrated cooling patent.8 Liquid hydrogen flows from the cryogenic tank (bottom) through a heat exchanger where it absorbs waste heat from the fuel cell, then through the fuel cell stack itself to generate electricity. Ambient air is compressed, intercooled, and fed to the fuel cell cathode. Note the number of subsystems surrounding the stack: compressor, intercooler, dual coolant loops, warming loop, and heat exchangers. This is the “balance of plant” that drives system-level power density well below the stack’s own 4 kW/kg — and every one of these components must work flawlessly in flight.

The second targets pressure energy recovery.9 The design uses an aeolipile — a Hero’s engine reaction turbine — to capture the energy of hydrogen depressurizing from cryogenic storage pressure to fuel cell inlet pressure. Multiple arms coupled to a shaft expel hydrogen through nozzles to spin a generator, with hydrodynamic bearings lubricated by the liquid hydrogen itself. Energy that every other hydrogen system wastes through a pressure regulator is converted to additional electrical output.

Both architectures are elegant. Both are direct reductions in balance-of-plant weight. And neither has been demonstrated at aviation scale.

A competitor benchmark deserves direct engagement. ZeroAvia announced in March 2023 that early testing of their HTPEM (High Temperature PEM) stack achieved 2.5 kW/kg at the cell level, and projected 3+ kW/kg at the system level within 24 months.10 If that projection had materialized, it would represent a significant bull-case data point — evidence that the 2 kW/kg barrier is not a law of nature but an engineering problem with a visible solution path.

That 24-month window closed in early 2025. As of this writing, no public announcement of a 3+ kW/kg system-level demonstration has followed. The gap between the projection and the silence that followed is itself instructive: it illustrates exactly the distance between cell-level laboratory results and integrated system performance. The balance of plant — compressor, cooling, water management, power electronics — is where weight accumulates and where projections go to die.

Even if ZeroAvia or another competitor eventually demonstrates 3+ kW/kg at the system level, it would not automatically validate Joby’s approach. ZeroAvia is targeting conventional fixed-wing aircraft retrofits with traditional cooling architectures. Joby’s duct-integrated, cryogenically coupled design is architecturally different and faces a distinct certification path. What we cannot determine from Joby’s patents is whether their specific architectures have been demonstrated in hardware at aviation-relevant scale and power.

V. THE CRYOGENIC ENGINEERING PROBLEM

Liquid Hydrogen at -253°C

The power density challenge assumes you can store liquid hydrogen on an aircraft in the first place. That is its own problem.

Liquid hydrogen is stored at 20 Kelvin — two degrees above absolute zero, the second-coldest liquid that can exist. The FAA’s December 2024 Hydrogen-Fueled Aircraft Safety and Certification Roadmap states plainly: cryogenic tanks “must maintain extremely low temperatures (20K), which requires very good insulation/thermal management. To avoid over-pressurization due to heating, cryogenic tanks need to be vented, a process commonly referred to as ‘boil-off.’”11 Unlike jet fuel, a sealed cryogenic tank will self-pressurize continuously as any heat leaks in. Venting must be engineered into the aircraft, adding weight and creating new failure pathways.

The NASA material selection study for liquid hydrogen cryotanks identifies a critical distinction between space applications and commercial aviation: space launch vehicles must survive approximately 10 thermomechanical cycles; commercial aircraft must survive on the order of 10,000 cycles.12 This is three orders of magnitude more demanding. The study notes that composite materials — the obvious choice for weight savings — suffer from hydrogen permeation, embrittlement, and potential delamination, and that airworthiness certification requirements for hydrogen-powered aircraft “are currently under development, therefore the merits of different designs are harder to establish.”12

The Aeolipile’s Specific Challenges

The aeolipile design9 is clever on paper but represents extraordinarily demanding engineering. The shaft is mounted via hydrodynamic bearings using liquid hydrogen as the lubricant. This means rotating machinery operating immersed in a fluid at -253°C, where most metals have become brittle, conventional seals have failed, and differential thermal expansion between components creates stress concentrations. The heat exchanger couples to and rotates with the shaft, and is specified as aluminum with a carbon-fiber overwrap — materials with very different thermal expansion coefficients undergoing continuous cryogenic cycling.

For context: the Space Shuttle Main Engine used liquid hydrogen turbopumps and required essentially artisanal manufacturing and inspection before every flight, at a cost of tens of millions of dollars per engine. Joby needs this to work reliably for thousands of cycles with a 20-minute commercial turnaround.

VI. THE THERMAL MANAGEMENT AND WEATHER PROBLEM

The power density and cryogenic challenges are about making the system light enough and cold enough. This section is about keeping it running once it is airborne — across every flight phase, every altitude, and every weather condition the aircraft might encounter.

Water: Too Much or Too Little

PEM fuel cells produce water as their only byproduct, and managing that water is a narrow and continuous control problem. The literature on PEMFC thermal management documents the core challenge: “if water is evaporated too slowly, it will flood the membrane and the accumulation of water inside the field flow plate will impede the flow of oxygen into the fuel cell, but if water evaporates too fast, the membrane will dry and the resistance across it increases.”13 Both failure modes reduce output power. Both also cause degradation.

This problem is flight-phase dependent and environment dependent. Research on PEM fuel cell systems for UAVs found that the relationship between cooling water flow rate, coolant bypass valve opening, and stack temperature varies non-linearly with flight altitude — and that each altitude has a different “safe working range” for the stack.14 The fuel cell control system must continuously navigate this operational envelope across the full flight profile: ground-level desert heat in Dubai at takeoff, sub-zero conditions at cruise altitude, and the power transients of vertical takeoff demanding maximum output at the worst possible time.

Cold Start and Icing

Below 0°C, the water produced by the cathode reaction freezes inside the cell. Research on PEMFC cold-start icing demonstrates that starting a PEM fuel cell from -15°C using a constant-voltage strategy leads to “quick failure of cold start due to severe icing in the cathode catalyst layer.”15 Ice formation causes volume expansion that physically damages the gas diffusion layer and catalyst layer — irreversible degradation, not merely a performance penalty.

For aircraft specifically, the literature notes that at sub-zero temperatures and high altitudes, ice formation “reduces stack voltage, prevents cold start, and causes irreversible degradation to the MEA” (membrane electrode assembly).16

A separate but related problem: Joby’s duct-integrated cooling design8 places diffuser vanes, heat exchangers, and variable area nozzles inside the propulsor fan ducts — complex internal geometry.

Cross-section of the propulsion duct from Joby’s cooling integration patent.8 Multiple heat exchanger elements are stacked inside the fan duct. Air enters from below, passes through the stacked heat exchangers, and exits through the duct opening. This is not a simple tube — it is a dense lattice of thermal hardware packed into the same duct that provides propulsive thrust. Every surface in this cross-section is an icing target.

In icing conditions, supercooled water droplets will accumulate on these surfaces. Conventional aircraft use bleed air from jet engines to anti-ice inlets. Joby has no jet engine. Their anti-icing heat source is the fuel cell waste heat that the duct-integrated cooling design8 is specifically trying to minimize. There is a direct physical tradeoff: every kilowatt used for anti-icing is a kilowatt not available for thrust.

The operational envelope is more constrained than it appears from ground-level testing. Analysis of PEM fuel cells in commercial aircraft confirms that system power output “is constrained by the compressor speed at high altitudes and the aftercooler cooling capacity at low altitudes” — and that “attainable inlet gas humidification limits high-altitude part load operation.”17

VII. THE BIRD STRIKE AND FOREIGN OBJECT DAMAGE PROBLEM

Standard FAA bird-strike certification tests require demonstrated containment or managed failure when a bird of specified mass impacts a fan or inlet at the aircraft’s operational speed. The physics are well-understood and the test protocols are established for conventional architectures.

Joby’s duct-integrated cooling design8 places a liquid hydrogen coolant loop inside the propulsor fan duct, radially outside the fan blades. A bird strike that damages a conventional fan blade produces a known class of failure. A bird strike that ruptures a heat exchanger carrying liquid hydrogen coolant inside a duct, adjacent to electrical components and rotating machinery, in a confined space, produces a failure mode that no existing certification framework addresses.

Cross-section of a propulsion duct from Joby’s high-altitude fuel cell patent,18 showing a heat exchanger mesh (hatched area) positioned directly in front of the propeller within the nacelle. Air entering the duct must pass through this mesh before reaching the fan. In a bird strike scenario, foreign object debris does not merely impact a rotating fan blade — it impacts a fragile thermal management structure containing hydrogen coolant, which then feeds debris into the fan. This is the architecture that must pass FAA bird-strike certification.

The safety properties of hydrogen make this particularly concerning. Hydrogen has a flammability range of 4%–75% in air — compared to jet fuel’s approximately 0.6%–6.5%.19 It has lower ignition energy, higher flame speeds, and greater detonation potential than conventional fuels.11 A hydrogen leak inside a duct that is also an air pathway needs only a small ignition source within a very wide concentration range to ignite.

The FAA’s hydrogen roadmap is explicit: “Hydrogen leakage is virtually unavoidable when there are fittings, couplings, joints, etc.”11 In Joby’s duct integration architecture,8 those fittings and couplings are inside the primary air pathway of the aircraft.

VIII. THE SAFETY CERTIFICATION ABYSS

No Framework Exists

Every challenge described above must ultimately pass through the FAA’s certification process. The problem is that the process does not yet exist.20

The FAA’s December 2024 roadmap acknowledges plainly: “Existing FAA airworthiness standards did not envision fuel cells, nor the use of hydrogen to fuel an aircraft engine.”11 This is not a bureaucratic delay — it is a fundamental absence of the technical and regulatory framework within which certification can occur.

The roadmap identifies that hydrogen aircraft certification will require developing entirely new standards for: crashworthiness of cryogenic tanks (thin-walled spherical tanks desirable for gravimetric efficiency “may not be adequate from a crashworthiness perspective”), fire suppression for hydrogen fires (hydrogen flames are colorless and nearly invisible in daylight), lightning protection (hydrogen’s low ignition energy makes requirements more stringent), and cold-start procedures at sub-zero airports.11

A 2025 MDPI safety assessment applied preliminary hazard analysis to liquid hydrogen storage systems across over 70 existing standards and guides, and identified that “the lack of prior experience with this technology, as well as the limited information on final system architecture, complicates performing such safety analyses.”21 The novel failure modes of Joby’s specific integrated architecture589 — hydrogen coolant loops inside fan ducts, aeolipile turbines using liquid hydrogen as bearing lubricant, variable area nozzles thermally integrated with the fuel cell — are not addressed by any existing standard.

The International Regulatory Picture

The scale of the certification gap becomes clearer in the April 2025 NAA Network Roadmap — a joint effort by the aviation authorities of five nations (US, UK, Australia, Canada, and New Zealand) to harmonize AAM type certification.22 The roadmap provides a concrete measure of how much of the certification basis is actually new: across five active FAA type certification applications for eVTOL aircraft, approximately 60% of the certification basis falls within existing regulations, while 40% requires entirely new airworthiness criteria still being written.22 That 40% figure is for battery-electric eVTOL aircraft. For a hydrogen fuel cell eVTOL, the proportion of new criteria is almost certainly higher — the roadmap identifies a dedicated workstream for hydrogen and hybrid-electric airworthiness requirements that does not even begin until January 2026, with a target completion of July 2026.22

Read that again: the international regulatory community has not yet started the formal process of developing the airworthiness standards that Joby’s hydrogen aircraft will need to be certified against. The work is scheduled to begin in 2026.

The roadmap’s own language is candid about the uncertainty: timelines for AAM certification “cannot yet be fully quantified given the nascent phase of AAM aircraft certification and operations.”22 The overall framework runs from July 2025 through July 2027 — a timeline that aligns almost exactly with Joby’s projected cash runway. The company is racing to certify an aircraft under standards that are being written on the same clock as its bank balance.

The Monte Carlo Risk Assessment

A 2026 Monte Carlo simulation-based risk assessment of hydrogen aviation ranks hydrogen leakage as the highest-risk category across all hydrogen aviation hazard domains, driven by “the gas’s extremely small molecular size, high diffusivity, and broad flammability range (4–75%), which collectively increase the probability of accidental ignition.”23 Cryogenic storage risks rank second, driven by “material embrittlement, insulation degradation, and rapid boil-off phenomena.” The study notes that these risks are not static — they compound under the operational cycling demands of commercial aviation.

IX. THE INFRASTRUCTURE AND OPERATIONS PROBLEM

Even if every engineering and certification challenge above is resolved, the aircraft needs fuel. Liquid hydrogen does not exist at airports.

The Supply Chain That Doesn’t Exist

Liquid hydrogen must be:

- Produced (electrolysis or reforming)

- Liquefied at

-253°C(energy-intensive, specialized equipment) - Transported in cryogenic tankers

- Stored in insulated cryogenic ground tanks

- Transferred to the aircraft through specialized cryogenic couplings

None of this infrastructure exists at any commercial airport today. The MIT analysis quantified the infrastructure requirements for hydrogen aviation across just five European countries in 2040: it requires a 36% increase in hydrogen generation capacity, approximately 100 GWh of combined liquid and gaseous storage, and adds 12% to total energy system costs.4 Joby’s Dubai air taxi operation would require purpose-built liquid hydrogen infrastructure at a single airport — infrastructure that does not exist and that Joby cannot build itself.

The economic burden is significant. Estimates suggest that adopting liquid hydrogen would increase direct operating costs by 10%–70% for short-range flights and 15%–102% for medium-range flights, driven primarily by storage and supply-chain demands.19

Turnaround Time

The FAA roadmap notes that liquid hydrogen lines will require purge during connection, maintenance, or refueling, and that space operations use helium as a purge gas — but “prodigious amounts would be required of this non-renewable resource to enable safe operation at airports.”11 The IATA Concept of Operations for hydrogen-powered aircraft identifies required new ground operations protocols including: detection of hydrogen leaks, ventilation requirements, inspection of hydrogen tanks and connectors, firefighting capability, and personal protective equipment for ground crews.24

The air taxi business model requires 10–15 minute turnarounds for economic viability. Cryogenic liquid transfer with purge requirements does not operate on that timeline without purpose-designed infrastructure that has never been built at a commercial airport.

X. THE VERTIPORT PROBLEM

Even if the aircraft works and the hydrogen supply chain materializes, the aircraft needs somewhere to land. In December 2025, Joby announced a partnership with Metropolis Technologies to develop 25 vertiports across the United States by converting parking garages in New York, Los Angeles, Miami, and San Francisco.25 The pitch: turn existing parking infrastructure into eVTOL hubs without building from scratch.

The engineering reality is considerably more involved.

The Power Problem

The same CoStar report that broke the Metropolis partnership noted, almost in passing, that vertiports require “up to 4,000 amps of clean electrical power.”25 This figure deserves more attention than it received. A large Manhattan residential tower typically draws 400–800 amps of total service. A 4,000-amp feed is a substation-level power delivery requirement — on a parking garage rooftop.

The underlying physics are straightforward: Joby’s S4 battery pack is approximately 220 kWh. To turn around an aircraft in 5–10 minutes — the pace required for commercial viability — demands charge rates on the order of 1–2 megawatts per pad. A multi-pad vertiport serving several simultaneous aircraft compounds this linearly. Retrofitting an existing parking structure requires a dedicated utility feed, step-down transformer, battery buffer storage to manage peak demand, and a high-voltage distribution system across the roof deck. None of this can be reused from the existing building electrical plant.

A related patent for eVTOL landing apparatus describes a charging assembly using high-voltage cable with magnetic induction, designed to connect automatically upon landing.26 But the patent is silent on where the upstream power comes from — the hardest and most expensive part of the problem.

Structural Loading and Rotor Downwash

A naive structural analysis would compare the weight of a Joby aircraft (~4,500 lbs) to a parked car (~3,500–4,500 lbs) and conclude the roof deck already handles equivalent loads. This misses the point. eVTOL downwash creates a distributed dynamic pressure load that is fundamentally different from a static point load. Six large rotors at high RPM during hover push air downward at high velocity, creating significant oscillating pressure across the landing area.

The patent literature shows the industry knows this. One vertiport design patent explicitly distinguishes between a solid deck — where downwash deflects laterally at hazardous velocity — and a “diffuser deck” consisting of perforated layers that convert high-velocity downwash into manageable airflow directed downward and outward.27 The diffuser deck exists specifically to solve two problems: reducing structural pressure loading and preventing rotor wash from creating dangerous conditions for ground crew and passengers. Adding one to an existing rooftop is not a minor retrofit — it requires installing a secondary elevated deck layer with perforation patterns calibrated to the specific aircraft’s rotor geometry.

The Regulatory Floor Is Still Moving

The FAA released its first vertiport design standard — Engineering Brief 105 — in September 2022,28 then quietly issued a significant update, EB 105A, on December 27, 2024, just weeks before the Joby-Metropolis announcement.29

EB 105A introduced a formal Downwash and Outwash Caution Area (DCA) around every landing zone, which must be managed for rotor wash hazards during operations. The FAA notes this may require “a significant amount of space” — potentially disqualifying smaller garage rooftops entirely.30 It also reclassified vertiports as a subclass of heliport, meaning they inherit the entire existing regulatory framework for heliports including obstacle clearance, approach surface geometry, and safety area standards.

Critically, the FAA has stated that EB 105A is not legally binding and will not serve as a standalone basis for enforcement — it is explicitly interim guidance pending a more comprehensive Advisory Circular.30 The standards Joby is designing to today may change, potentially requiring costly retrofits to early builds.

And there is a harder problem beneath the standards: every vertiport must have FAA-approved approach and departure corridors. In New York, the airspace around JFK, LaGuardia, and Newark creates large volumes of restricted airspace that complicate low-altitude urban operations considerably.28 A parking garage that is structurally suitable and electrically upgradeable may still be unusable if no viable approach corridor exists from any direction. Airspace certification is likely the longest-lead-time element of the entire vertiport buildout — and Joby cannot control the timeline.

XI. WHY THE RISKS COMPOUND

Each challenge above is a hard problem independently. The more important analytical point is how they interact.

These are not engineering problems that can be solved sequentially — they must be solved simultaneously in an integrated system, under aviation certification standards where the acceptable failure rate is measured in events per billion flight hours. And they trade off against each other:

- Solving the thermal management problem well (hotter fuel cells, better heat rejection) helps icing resistance but increases balance-of-plant weight, working against the

2 kW/kgtarget. - Adding redundancy to the hydrogen containment system to address bird strike and leak risks adds weight, working against the

2 kW/kgtarget. - Making the aeolipile turbine more maintainable by simplifying its design reduces energy recovery efficiency, working against range and economics.

- Designing the cryotank for

10,000thermomechanical cycles rather than the10cycles of space applications requires heavier, more conservative materials, working against the tank gravimetric index target. - Addressing cold-start icing with dedicated heating draws power away from propulsion during the highest-power-demand phase of flight (vertical takeoff).

- Building vertiports with the

4,000-amp electrical feeds needed for fast charging requires capital expenditure that competes with R&D spending, while the FAA’s vertiport design standards remain interim and subject to change.2930

Every solution to one problem creates or worsens another. And the timeline compounds it all: the international regulatory roadmap for AAM certification runs through July 2027,22 the hydrogen-specific airworthiness workstream doesn’t start until 2026,22 and Joby’s cash runway — at its current burn rate — expires on roughly the same schedule. There is no margin for the kind of iterative development that novel aerospace programs historically require.

XII. WHAT THE PATENTS TELL US — AND WHAT THEY DON’T

Joby’s patent portfolio shows genuine engineering depth. The foundational thermodynamic integration approach5 is consistent with what the MIT analysis identifies as necessary to achieve 2 kW/kg. The waste heat recovery architecture8 and the pressure energy recovery design9 are the right architectural moves to reduce balance-of-plant weight. The inventors understand the literature, and the claims target the correct bottlenecks.

What the patents cannot tell us:

- Whether these systems have been demonstrated in hardware at aviation-relevant scale and power

- Whether the aeolipile turbine survives the thermomechanical cycling of commercial aviation

- What specific power the integrated system actually achieves

- Whether the FAA will certify the duct-integrated cooling architecture before or after a bird strike test program is defined and completed

- Whether liquid hydrogen infrastructure at Dubai International Airport will be operational before Joby’s current cash runway expires

What Could Prove Us Wrong

This analysis identifies risks. Risks are not certainties. Several developments could meaningfully change the picture.

A breakthrough in balance-of-plant weight reduction. If Joby’s integrated cooling and pressure-recovery architectures deliver the weight savings they promise on paper, the 2 kW/kg target may be achievable without further innovation. The architectures are sound in principle. We simply have no public evidence they work in practice.

Faster-than-expected regulatory progress. The FAA could adopt a special condition or equivalent safety finding approach that allows certification to proceed in parallel with standards development, rather than waiting for complete frameworks. The agency has done this for novel aircraft types before, though never for anything this far from the existing fleet.

Hybrid architectures as a bridge. Recent research has proposed hybrid fuel cell systems with aluminum-air battery backup for emergency reserves,31 which could relax the specific power requirements on the primary fuel cell by providing a safety margin through a secondary system. If Joby is pursuing something similar, the 2 kW/kg threshold might not need to be hit cleanly.

Strategic partnerships for infrastructure. If a sovereign wealth fund or energy company commits to building liquid hydrogen infrastructure at a flagship airport — Dubai being the obvious candidate — the infrastructure timeline could compress from decades to years.

None of these are implausible. All of them require events that have not yet occurred.

The Bottom Line

The patents are impressive. The physics is hard. The certification path is undefined. The infrastructure does not exist. And the challenges don’t just stack — they interact, trading off against each other in ways that make the integrated problem harder than the sum of its parts.

This is not a judgment on whether Joby will succeed. It is a map of what success requires. Any investor in this company should understand these risks clearly, because the market is pricing a future that depends on every one of them being resolved — simultaneously, at scale, under certification standards that have not been written, before the money runs out.

SOURCE INDEX

| Source | Type | Key Finding |

|---|---|---|

| US 11,565,607 (Joby Aero, 2023) | Patent | Foundational thermodynamic fuel cell architecture; Bevirt listed as inventor |

| US 12,515,806 (Joby Aero, 2026) | Patent | Duct-integrated cooling; fuel cell waste heat recovered as thrust |

| US 12,276,210 (Joby Aero, 2025) | Patent | Aeolipile hydrogen expansion turbine; LH2 hydrodynamic bearings |

| US 12,077,064 (Joby Aero, 2024) | Patent | High-altitude thermodynamic fuel cell system; full process flow with water/ice management |

| US 2026/0051518 (Joby Aero, 2026) | Patent Application | Pressurized fuel cell system; detailed pressure vessel with coolant and humidifier integration |

| Cybulsky et al., arXiv:2309.14629 (MIT, 2023) | Academic | 2 kW/kg system power + 50% tank GI required for viable hydrogen regional aviation |

| Datta, NASA CR-20210000284 (2021) | Technical Report | 1.1 kW/kg minimum system target for eVTOL; cooling and storage as key drivers |

| ATI Fuel Cells Roadmap (2022) | Industry | PEM stacks at 4 kW/kg stack-level; balance of plant is the system-level barrier |

| ZeroAvia HTPEM announcement (2023) | Industry | 2.5 kW/kg cell-level demonstrated; 3+ kW/kg system-level projected |

| FAA Hydrogen-Fueled Aircraft Safety Roadmap (Dec 2024) | Regulatory | No existing airworthiness standards for hydrogen aircraft; certification frameworks TBD |

| Liang et al., Advanced Science (2023) | Academic | Cold start failure and irreversible MEA degradation from icing below 0°C |

| Heliyon PEMFC thermal review (2024) | Academic | Water flooding/drying tradeoff; cold-start failure mechanisms |

| ScienceDirect PEM UAV study (2022) | Academic | Altitude-dependent safe operating envelope; water-thermal management complexity |

| ScienceDirect HT-PEMFC aircraft review (2024) | Academic | Sub-zero membrane degradation; TMS architecture options for aviation |

| ScienceDirect PEM operating analysis (2021) | Academic | Power output constrained by compressor speed at altitude, aftercooler capacity at low altitude |

| MDPI Aerospace LH2 safety assessment (2025) | Academic | Preliminary hazard analysis; material embrittlement, boil-off as key risks |

| MDPI Aerospace Monte Carlo risk (2026) | Academic | Leakage highest-risk category (4–75% flammability range); cryogenic storage second |

| NASA-TM-20250007133 cryotank materials (2025) | Technical Report | 10,000 thermomechanical cycles required vs. 10 for space; certification standards absent |

| Wiley Advanced Energy review (2025) | Academic | LH2 increases operating costs 10–70%; hydrogen flammability range 4–75% in air |

| SKYbrary Hydrogen Certification (2025) | Regulatory | Comprehensive summary of FAA/EASA certification gaps |

| Kaushik et al., arXiv:2509.23682 (2025) | Academic | Hybrid fuel cell + Al-air backup architecture for emergency reserves |

| IATA Concept of Operations (2025) | Industry | Ground operations protocols for hydrogen-powered aircraft |

| CoStar News / Scheier (Dec 2025) | Industry | Joby-Metropolis partnership; 25 vertiports; 4,000-amp power requirement |

| WO 2024/118,965 (Johnson, 2024) | Patent | eVTOL landing apparatus with high-voltage induction charging |

| WO 2024/155,749 (Edgette, 2024) | Patent | Vertiport diffuser deck design; passenger sequencing; stowable railings |

| FAA Engineering Brief 105 (Sep 2022) | Regulatory | First US vertiport design standard; TLOF/FATO/Safety Area geometry |

| FAA Engineering Brief 105A (Dec 2024) | Regulatory | Downwash Caution Area; vertiport reclassified as heliport subclass; interim guidance |

| Jetlaw EB 105A Analysis (Jan 2025) | Legal | EB 105A not legally binding; final Advisory Circular pending |

| NAA Network AAM Roadmap (Apr 2025) | Regulatory | 60/40 certification split; hydrogen workstream Jan–Jul 2026; 5-nation harmonization |

| American Airlines Group 10-Q (2024–2025) | SEC Filing | ~$54B annual revenue at comparable ~$10B market cap; 0.19x P/S vs. JOBY’s 100x+ |

| Joby Aviation / Blade Acquisition (Aug 2025) | Press Release | Blade passenger business acquired for up to $125M; 12 terminals; 50K+ passengers in 2024 |

| Blade Air Mobility Q4 2024 Results (Mar 2025) | SEC Filing | Passenger segment revenue $102M in 2024; short-distance $72M; medical ($147M) excluded from Joby deal |

All patent citations reference publicly available USPTO records. All academic citations reference peer-reviewed or preprint literature.

Joby Aviation. (2025, August 4). “Joby to Acquire Blade’s Passenger Business, Accelerating Air Taxi Commercialization.” Press release. Acquisition of Blade’s passenger business for up to $125M in stock or cash, including 12 urban terminals (JFK, Newark, three Manhattan locations) and the Blade brand. Blade flew more than 50,000 passengers in 2024. Medical division excluded and remains a separate public company. ↩︎ ↩︎

Blade Air Mobility. (2025, March 13). “Blade Air Mobility Announces Fourth Quarter 2024 Results.” Press release. Full-year 2024 passenger segment revenue of $101.9M ($72.2M short-distance, $29.7M jet and other). Total company revenue of $248.7M; medical segment revenue of $146.8M not included in Joby acquisition. ↩︎

American Airlines Group (AAL) SEC-filed 10-Q quarterly reports (2024–2025). Revenue of approximately $54B annualized based on Q1–Q3 2025 filings ($40.6B through three quarters). Market capitalization of approximately $10B as of February 2026. Fleet, employee, and passenger figures from AAL 2024 10-K. ↩︎

Cybulsky, A. et al. (2023). “Hydrogen-Powered Aircraft: A Techno-Economic Analysis of Fuel Cell and Battery Systems for Regional Aviation.” arXiv:2309.14629. Massachusetts Institute of Technology. ↩︎ ↩︎

US 11,565,607. High Efficiency Hydrogen Fueled High Altitude Thermodynamic Fuel Cell System and Aircraft Using Same. Mikic, Bevirt, Lynn, Stoll. Filed June 2021, granted January 2023. Joby Aero, Inc. ↩︎ ↩︎ ↩︎

UK Aerospace Technology Institute. (2022). Fuel Cells for Aerospace Applications: Technology Roadmap. PEM stacks at 4 kW/kg stack-level; balance of plant (air supply, heat rejection, water management) identified as weight-limiting subsystem driving system-level performance to 0.65–1 kW/kg. ↩︎ ↩︎

Datta, A. (2021). Fuel Cell Study for eVTOL. NASA CR-20210000284. Concluded 1.1 kW/kg system-level specific power as the minimum target for fuel cell eVTOL to match piston-engine rotorcraft performance. ↩︎

US 12,515,806. Aircraft Propulsion System with Integrated Fuel Cell Cooling. Brelje, Lynn, Lotterman, Mikic. Filed December 2023, granted January 2026. Joby Aero, Inc. ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

US 12,276,210. Hydrogen Expansion System for Fuel Cell Use. Lynn, Lotterman. Filed December 2023, granted April 2025. Joby Aero, Inc. ↩︎ ↩︎ ↩︎ ↩︎

ZeroAvia. (2023, March). HTPEM (High Temperature PEM) stack testing announcement: 2.5 kW/kg at cell level, with system-level projection of 3+ kW/kg within 24 months. ↩︎

Federal Aviation Administration. (2024, December). Hydrogen-Fueled Aircraft Safety and Certification Roadmap. Identifies fundamental gaps in existing airworthiness standards for hydrogen aircraft and outlines required new standards for crashworthiness, fire suppression, lightning protection, and ground operations. ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

NASA-TM-20250007133 (2025). Material selection study for liquid hydrogen cryotanks. Documents the 10,000-cycle commercial aviation requirement versus ~10 cycles for space launch, and identifies composite material challenges including hydrogen permeation and embrittlement. ↩︎ ↩︎

Comprehensive review of PEMFC thermal management. Heliyon (2024). Documents water flooding/drying tradeoff and cold-start failure mechanisms in PEM fuel cells. ↩︎

PEM fuel cell systems for UAVs. ScienceDirect (2022). Found altitude-dependent safe operating ranges for fuel cell stack temperature, cooling water flow, and coolant bypass valve settings. ↩︎

Liang, D. et al. (2023). “Cold Start Icing in PEM Fuel Cells.” Advanced Science. Demonstrated that constant-voltage cold start from -15°C leads to rapid failure from cathode catalyst layer icing, with irreversible MEA degradation. ↩︎

HT-PEMFC aircraft review. ScienceDirect (2024). Documents sub-zero membrane degradation and thermal management system architecture options for aviation fuel cell applications. ↩︎

Operating analysis of PEM fuel cells in commercial aircraft. ScienceDirect (2021). Confirmed that power output is constrained by compressor speed at high altitude and aftercooler capacity at low altitude. ↩︎

US 12,077,064. High Efficiency Hydrogen Fueled High Altitude Thermodynamic Fuel Cell System and Aircraft Using Same. Mikic, Bevirt, Lynn, Stoll. Filed July 2023, granted September 2024. Joby Aero, Inc. ↩︎

Hydrogen properties and aviation economics review. Wiley Advanced Energy and Sustainability Research (2025). Documents hydrogen flammability range of 4–75% in air and estimates liquid hydrogen adoption increases operating costs 10–70% for short-range, 15–102% for medium-range flights. ↩︎ ↩︎

SKYbrary Aviation Safety. (2025). “Hydrogen-Fueled Aircraft — Certification.” Comprehensive summary of FAA/EASA certification gaps for hydrogen aviation. ↩︎

MDPI Aerospace (2025). Preliminary hazard analysis of liquid hydrogen storage systems applied across 70+ existing standards. Identified limited prior experience and undefined system architecture as key complications for safety analysis. ↩︎

NAA Network. (2025, April). Network Roadmap for Advanced Air Mobility Aircraft Type Certification, Edition 1.0. Joint publication of FAA, UK CAA, CASA (Australia), TCCA (Canada), and CAA NZ. Reports 60/40 split between existing CFR and new airworthiness criteria across five active FAA type certification applications. Identifies dedicated hydrogen/hybrid-electric airworthiness workstream scheduled January–July 2026. Notes timelines “cannot yet be fully quantified given the nascent phase of AAM aircraft certification and operations.” ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

MDPI Aerospace (2026). Monte Carlo simulation-based risk assessment of hydrogen aviation. Ranked hydrogen leakage as highest-risk category due to small molecular size, high diffusivity, and broad flammability range. Cryogenic storage ranked second. ↩︎

IATA. (2025). Concept of Operations for Hydrogen-Powered Aircraft. Identifies required ground operations protocols including leak detection, ventilation, tank inspection, firefighting, and crew PPE requirements. ↩︎

Scheier, R. (2025, December 24). “California startups join forces to turn US parking lots into flying taxi stations.” CoStar News. Reports 4,000-amp power requirement and Joby-Metropolis partnership for 25 US vertiports. ↩︎ ↩︎

WO 2024/118,965 A1. Aircraft Takeoff and Landing Apparatus. Johnson, K. Published June 2024. Describes high-voltage magnetic induction charging assembly for eVTOL aircraft. ↩︎

WO 2024/155,749 A1. Infrastructure Suitable for VTOL Aircraft Network and VTOL Aircraft Therefor. Edgette, C. Published July 2024. Describes diffuser deck design, passenger sequencing, and stowable safety railings. ↩︎

FAA Engineering Brief No. 105, Vertiport Design. September 2022. First formal US vertiport design standard establishing TLOF, FATO, and Safety Area geometry requirements. ↩︎ ↩︎

FAA Engineering Brief No. 105A, Vertiport Design — Supplemental Guidance. December 27, 2024. Introduced Downwash and Outwash Caution Area (DCA), reclassified vertiports as heliport subclass. ↩︎ ↩︎

Jetlaw. (2025, January 15). “FAA Updates EB 105A: Vertiport Design Standards.” Analysis noting EB 105A is explicitly interim guidance, not legally binding, pending forthcoming Advisory Circular. ↩︎ ↩︎ ↩︎

Kaushik, S. et al. (2025). “Hybrid Fuel Cell Architecture with Aluminum-Air Backup for Emergency Reserves.” arXiv:2509.23682. Proposes hybrid fuel cell + Al-air battery architecture as a potential safety backup for hydrogen aviation. ↩︎